What is an Irrevocable Trust?

Estate planning is an important part of financial management that ensures one’s assets are managed and distributed according to their wishes upon their death. Estate planning encompasses a broad range of strategies aimed at preserving wealth, reducing tax liabilities, and protecting assets from creditors. Irrevocable trusts are one tool that can offer a level of permanence and protection that can be perfect for individuals with significant assets or specific planning needs.

With the increasing complexity of tax laws, the rising costs of healthcare, and the growing need for asset protection, irrevocable trusts provide a solution that addresses these concerns comprehensively. Here’s everything you need to know!

Irrevocable Trusts as Permanent Legal Entities

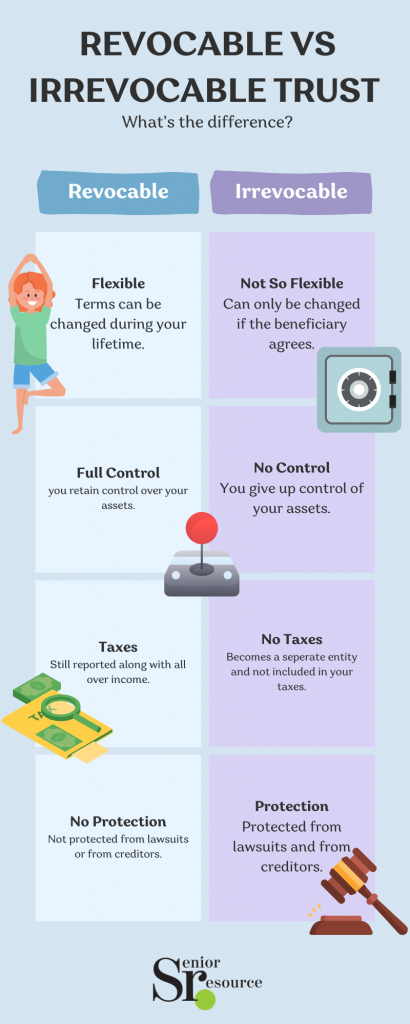

An irrevocable trust is a legal arrangement in which the grantor, the individual who creates the trust, permanently transfers assets into the trust. Once assets are placed in an irrevocable trust, the grantor cannot modify, revoke, or reclaim them. This permanence differentiates irrevocable trusts from revocable trusts, where the grantor retains the ability to alter or dissolve the trust.

Irrevocable trusts are established through a formal legal document that outlines the terms and conditions under which the trust will operate. This document specifies the roles and responsibilities of the grantor, trustee, and beneficiaries. The irrevocable nature of the trust ensures that the assets are protected from external claims and that the grantor’s wishes are adhered to without the possibility of future alteration.

Primary Objectives of Irrevocable Trusts

The primary objective of an irrevocable trust is to protect and preserve assets. By transferring ownership of assets to the trust, the grantor removes these assets from their personal estate. This action provides several key benefits, including shielding assets from creditors, reducing estate taxes, and qualifying for government benefits such as Medicaid.

Asset protection is an important consideration for those with substantial wealth or those exposed to potential legal liabilities. An irrevocable trust effectively places assets out of reach of creditors, ensuring that they remain intact for the benefit of the beneficiaries. Additionally, the reduction in estate taxes can be significant, especially for high-net-worth individuals. By removing assets from the taxable estate, the trust helps minimize the overall tax burden, allowing more wealth to be transferred to future generations.

Irrevocable trusts also play a role in Medicaid planning. As healthcare costs continue to rise, qualifying for Medicaid can be essential for covering long-term care expenses. By transferring assets to an irrevocable trust, individuals can meet the Medicaid eligibility requirements while preserving their wealth for their heirs. This strategy allows for the efficient management of healthcare costs without depleting personal assets.

Key Elements of an Irrevocable Trust

“Grantor,” the Creator of the Trust

The grantor is the person who establishes the trust and transfers assets into it. In doing so, the grantor gives up all ownership rights and control over these assets, ensuring they are managed according to the trust’s terms. This relinquishment of control is a fundamental aspect of irrevocable trusts and is necessary for achieving their intended benefits.

“Trustee,” Person or Entity Responsible for Managing Trust Assets

The trustee is the person or entity appointed to manage the trust’s assets. The trustee is responsible for ensuring the trust operates according to its terms and serves the best interests of the beneficiaries. Trustees can be individuals, professional trust companies, or financial institutions.

“Beneficiary,” Recipient of Trust Assets

Beneficiaries are the individuals or entities entitled to receive the benefits from the trust. The grantor specifies the beneficiaries and the terms under which they will receive distributions in the trust document. Beneficiaries can include family members, friends, charitable organizations, or any other entities the grantor wishes to benefit.

“Irrevocability,” Nature of the Trust Being Unchangeable Once Established

The irrevocability of the trust means that once it is created and funded, the grantor cannot alter or revoke it. The permanent nature of the trust ensures that the grantor’s wishes are preserved and cannot be changed by future events or decisions.

“Terms and Conditions,” Specific Instructions for Asset Distribution and Management

The trust document outlines specific terms and conditions for managing and distributing the trust’s assets. These terms are legally binding and must be followed by the trustee. The terms can include instructions for how the assets are to be invested, when and how distributions are to be made to beneficiaries, and any other conditions the grantor wishes to impose.

Benefits and Considerations

Asset Protection

One of the most significant benefits of an irrevocable trust is asset protection. By transferring assets to the trust, the grantor shields them from creditors and legal claims. Since the grantor no longer owns the assets, they cannot be targeted in lawsuits or debt collections.

Tax Efficiency

Irrevocable trusts can also provide substantial tax benefits. By removing assets from the grantor’s estate, the trust can help reduce estate taxes. Additionally, certain types of irrevocable trusts can provide income tax advantages, depending on how they are structured.

Estate tax reduction is a primary consideration for high-net-worth individuals. By transferring assets to an irrevocable trust, the grantor can lower the taxable value of their estate, potentially saving significant amounts in estate taxes. This strategy allows more wealth to be passed on to future generations, preserving the family’s financial legacy.

Medicaid Planning and Long-Term Care Benefits

Irrevocable trusts are commonly used in Medicaid planning. By transferring assets to an irrevocable trust, individuals can qualify for Medicaid benefits while preserving their wealth for their beneficiaries. This strategy is particularly valuable for covering long-term care costs without depleting personal assets.

Permanence

The irrevocability of the trust ensures that the grantor’s wishes are preserved and cannot be altered by future changes in circumstances or legal challenges. This permanence provides peace of mind that the assets will be managed and distributed as intended.

Types of Irrevocable Trusts

Insurance Trusts

A life insurance trust is designed to hold life insurance policies. Upon the grantor’s death, the proceeds from the life insurance policy are paid into the trust, rather than directly to the beneficiaries.

Tax Benefits and Asset Protection

Life insurance trusts offer significant tax benefits. By placing a life insurance policy in an irrevocable trust, the proceeds are excluded from the grantor’s estate, reducing estate taxes. Additionally, the trust can provide asset protection, ensuring the proceeds are managed and distributed according to the grantor’s wishes.

Charitable Trusts

Charitable trusts are established to benefit charitable organizations. These trusts can provide immediate tax deductions for the grantor and allow for philanthropic giving in a structured manner.

Support for Philanthropic Causes

Charitable trusts enable grantors to support their chosen causes and organizations. They can be structured to provide income to the grantor or other beneficiaries for a period before the remaining assets are distributed to the charity.

The Bottom Line on Irrevocable Trusts

For those looking to secure their financial future and protect their assets, exploring the benefits of irrevocable trusts is a worthwhile endeavor. With proper planning and professional guidance, an irrevocable trust can provide peace of mind and long-term security for both the grantor and their beneficiaries.

Popular Articles About Trusts

Originally published July 15, 2024